Practically 68 million folks within the U.S. had been going through excessive climate alerts as of Aug. 7 — that’s about one-fifth of the U.S. inhabitants. Attributable to local weather change, extra folks expertise hazardous climate situations like excessive warmth, wildfires, storms and floods, they usually expertise them extra typically. Some locations are extra weak to local weather change’s impression than others, however that doesn’t cease folks from shifting to these spots.

A brand new evaluation by NerdWallet finds that almost all of the fastest-growing locations within the U.S. are additionally high-risk areas for pure hazards.

“Excessive warmth and humidity goes to be a actuality just about irrespective of the place you progress,” says Alex De Sherbinin, senior analysis scientist, deputy director and adjunct professor of local weather on the Columbia Local weather Faculty at Columbia College in New York. “However life-threatening damages from these sorts of issues are going to be extra restricted to some locales than others.”

You’re extra more likely to expertise excessive climate proper now than at another time of 12 months. That’s as a result of the U.S. is in its “hazard season,” the interval between Might and October when North America experiences its worst local weather impacts, in accordance with the Union of Involved Scientists, a nonprofit advocacy group.

The summer season, to date, has been brutal. June was the most popular month on report for your complete planet till July broke that report, in accordance with the Copernicus Local weather Change Service, a program organized and funded by the European Union, member states and associated businesses.

Within the U.S., the South baked from oppressive warmth; the floor water temperature off the coast of Florida reached 101 levels Fahrenheit; and Loss of life Valley sweltered at 128 levels Fahrenheit — the most popular day on report. As well as, floods drowned components of New England, and Canada’s worst-ever wildfire season remains to be anticipated to choke the northern half of the united stateswith smoke periodically till the primary snowfall.

These are simply the fast results of our local weather emergency. Predicted long-term results embrace sea-level rise by as a lot as 10 to 12 inches within the 30-year interval between 2020 and 2050, the identical rise that was measured over a 100-year interval from 1920 to 2020, in accordance with a 2022 report by the Nationwide Oceanic and Atmospheric Administration.

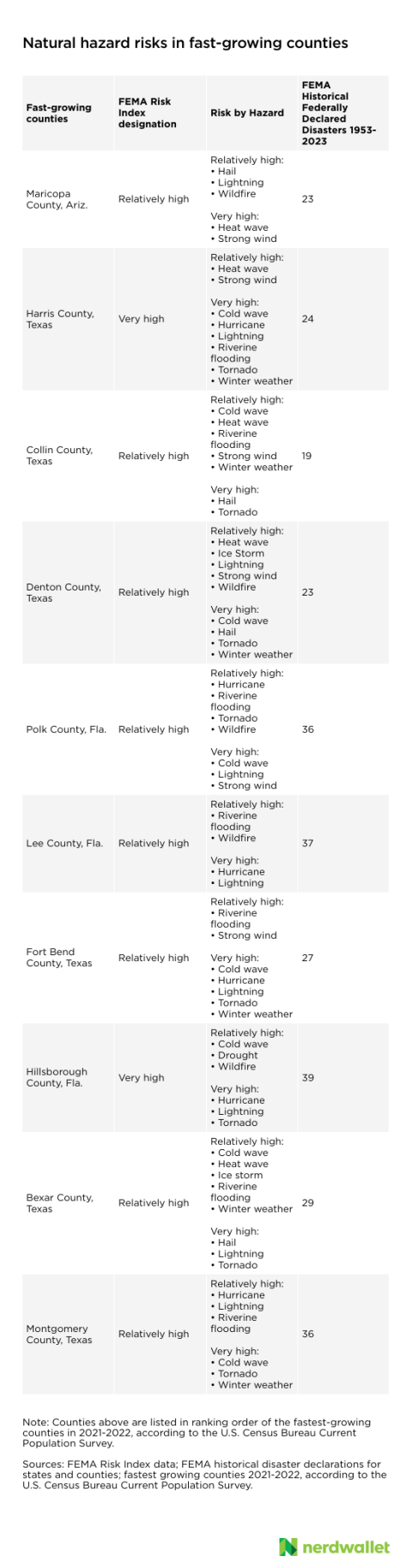

Quick-growing locations are at excessive danger for worsening local weather situations

Among the many 10 fastest-growing counties, two are thought-about at very excessive danger for pure hazards and eight are thought-about at comparatively excessive danger for pure hazards. Not one of the fastest-growing counties are thought-about at comparatively reasonable danger or low danger.

An individual ready for the subway wears a filtered masks as smoky haze from wildfires in Canada blankets a neighborhood on June 7 within the Bronx borough of New York Metropolis. (Picture by David Dee Delgado/Getty Photos)

For context, of the three,231 counties the Federal Emergency Administration Company (FEMA) danger index covers, 15 are thought-about at very excessive danger (0.46%); 129 are thought-about at comparatively excessive danger (3.99%); and 397 are thought-about at comparatively reasonable danger (12.29%).

All the fastest-growing counties are situated within the western or southern components of the U.S., together with six counties in Texas, three in Florida and one in Arizona.

Every of the counties carries its personal potential hazards: hurricanes in all three counties in Florida; warmth waves in Maricopa County, Arizona; and a near-biblical assortment of dangers within the Texas counties, together with chilly waves, warmth waves, hurricanes, tornadoes, wildfires and extra.

There have been 4,762 federally declared disasters within the U.S. since 1953, in accordance with FEMA information. Every of the fastest-growing counties has had its fair proportion of federally declared disasters within the final 70 years. Hillsborough County, Florida, had probably the most occasions (39), adopted carefully by Lee County, Florida (37), and Montgomery County, Texas (36). In every of those counties, tropical storms had been the reason for the disasters.

Warming sea floor temperatures on account of local weather change trigger hurricanes which are bigger, have extra intense wind speeds and better precipitation, in accordance with the Heart for Local weather and Power Options, an environmental coverage suppose tank.

What occurs once you transfer to a high-risk space

Normally, shifting from one place to a different is closely age-dependent, says De Sherbinin. Youthful folks are usually extra cellular as they set up their careers, and have a tendency to cool down after they have a household. Older folks migrate on the finish of their careers as a result of they wish to retire someplace close to household or have facilities they worth most.

“These classical motivations have been comparatively impervious to the sense that there’s a rising danger that we face as a society,” says De Sherbinin.

Prioritizing your way of life and profession preferences over avoiding excessive ecological dangers is solely human nature, says De Sherbinin. Why? Individuals don’t essentially suppose disaster will occur to them.

De Sherbinin says once you transfer to an space that’s extremely weak to local weather change results, the rationalization normally goes one thing like this: “‘I’m not going to be the one to lose my home over the cliff into the Pacific Ocean, as a result of I’m simply fortunate.’”

The U.S. tends to be an outlier relating to folks shifting into areas the place dangers are actually excessive, says De Sherbinin, who research the human features of world environmental change. However the larger the danger of pure hazards, the extra weak the inhabitants is to direct and secondary impacts of climate occasions. Direct impacts are extra fast bodily hurt and property hurt, whereas secondary impacts are usually longer-term, akin to financial loss, social unrest and probably a retreat from the world.

As said earlier, local weather change is worsening the probability and the acute nature of climate occasions, which suggests these excessive dangers could manifest in an actual means and extra typically.

Andrea Washington weeps after pouring water on herself within the Hungry Hill neighborhood on July 11 in Austin, Texas. Washington started to cry as she spoke in regards to the warmth and her well being. (Picture by Brandon Bell/Getty Photos)

For instance, the acute warmth situations in Texas not too long ago had been made considerably extra probably by local weather change, in accordance with the U.S. Local weather Shift Index (CSI) Map. Intense warmth in Houston, the county seat for Harris County — the second fastest-growing county in accordance with the Census Bureau — is now 5 instances extra widespread on account of local weather change, in accordance with the CSI Map. With out local weather change, excessive warmth would in any other case be uncommon for that space, in accordance with the CSI scale.

About 80% of the U.S. inhabitants lives in cities the place “warmth island” results exacerbate excessive warmth situations. Among the many 44 main cities analyzed by Local weather Central, a nonprofit science and information group, 9 have greater than 1 million individuals who really feel at the very least Eight levels Fahrenheit hotter as a result of city surroundings. Amongst these 9 cities, three are within the fastest-growing counties listed on this evaluation. Houston is on the checklist, in addition to Phoenix in Maricopa County, Arizona, and San Antonio in Bexar County, Texas.

Climate-battered locations could develop into uninsurable

Shifting to an space that’s at excessive danger for pure hazards could price you greater than you bargained for, in additional methods than one, starting with property insurance coverage.

Insurance coverage giants State Farm and Allstate not too long ago introduced that they’re now not issuing new house owner insurance policies in California. State Farm cites “quickly rising disaster publicity” amongst its causes for pulling again.

Loretta Worters, vice chairman of media relations for the Insurance coverage Info Institute, says the business is at a pivotal level as a complete. Insurers are creating methods to raised perceive the dangers of maximum climate occasions, however it’s getting tougher to cost danger, she says. It additionally prices shoppers extra to get insurance coverage as a result of the dangers are so nice, Worters says.

“Everyone desires this idyllic form of way of life; we wish to be on the coast or we wish to be in these stunning, serene areas the place there’s a lot of shrubbery and privateness,” says Worters. “However you may’t get hearth vans in — into areas which are liable to wildfires. A number of these folks’s houses are located such that it is onerous for the vans to rise up there as a result of they’re on winding roads.”

California isn’t the one state the place insurance coverage could also be onerous to return by on account of power climate occasions. Flood-prone states have lengthy felt the sting of rising charges and problem getting protection. A not too long ago rolled-out change to the Nationwide Flood Insurance coverage Program (NFIP) is making it much more costly. This system is usually the one one accessible in flood-prone areas.

FEMA says the speed will increase, referred to as “Threat Score 2.0,” will allow the company to distribute premiums and set charges which are extra equitable than previously. The brand new methodology assesses extra variables than it used to love flood frequency, forms of flooding, the property’s distance to a water supply in addition to its elevation, and prices to rebuild.

On June 1, a bunch of 10 states joined a go well with led by Louisiana Lawyer Gen. Jeff Landry in opposition to FEMA, the Division of Homeland Safety and the Federal Insurance coverage and Mitigation Administration in an try to dam steep price will increase to the NFIP that went absolutely into impact on April 1. The states — which embrace Florida, Idaho, Kentucky, Louisiana, Mississippi, Montana, North Dakota, South Carolina, Texas and Virginia — argue the upper charges may power policyholders to drop their protection or find yourself surrendering their houses and companies.

Insurance coverage prices have climbed in the previous few many years: Insured disaster losses have elevated by almost 700% because the 1980s when adjusted for inflation, in accordance with the Insurance coverage Info Institute. And in 2021, insured losses from pure catastrophes totaled $130 billion — 76% larger than the 21st-century common.

If extra insurers pull out of areas on account of power climate situations like wildfires and hurricanes, areas may develop into astronomically costly to insure, if not altogether uninsurable. Fewer personal insurers accessible means householders will probably want to show to Honest Entry to Insurance coverage Necessities (FAIR) plans. All states have some kind of a plan, which is instituted on the state stage and backed by personal insurers licensed to write down insurance coverage within the state. All the corporations have a proportionate share in any earnings, losses and bills of the plans.

FAIR plans normally supply solely fundamental protection and are used “as a final resort,” in accordance with the Nationwide Affiliation of Insurance coverage Commissioners (NAIC), a nonprofit regulatory help group.

Worters, of the Insurance coverage Info Institute, says FAIR plans are more likely to have larger deductibles and fewer protection, they usually could also be tougher to acquire. Nonetheless, they’re broadly used: 10% of Florida householders have insurance coverage by the state’s FAIR plan, the Residents Property Insurance coverage Corp., as of March 2022, in accordance with the NAIC.

Individuals kayak up and down the flooded waters of Elm Avenue on July 11 in Montpelier, Vermont. (Picture by Kylie Cooper/Getty Photos)

Rising charges are a supply of tension and frustration for policyholders, says Worters, however she provides that the insurance coverage business isn’t the one social gathering that should reply to worsening local weather situations. Property dangers will be mitigated, she says, by coverage and property safeguards akin to constructing codes in hurricane-prone areas or defensible area necessities — buffers round property — in wildfire-prone areas.

“We’re insuring it, however if you happen to proceed to dwell in these areas and also you don’t take any measures to safeguard your own home or your online business, it simply makes issues worse.”

Stephanie Pincetl, founding director and professor on the California Heart for Sustainable Communities at UCLA, says altering how we dwell might be essential to combating the impacts of local weather change. “I believe that we have to understand the American sample of land use contributes 100% in the direction of local weather change and in addition has tons and many different ramifications. And we now have not been coping with that,” says Pincetl. “We’ve got giant homes, we now have many loos, we now have personal gardens and so forth. And people are inherently energy-intensive, land-intensive and water-intensive.”

Will folks migrate on account of local weather change?

If local weather situations worsen in your space, you’ll inevitably be confronted with this conundrum: Ought to I keep, or ought to I’m going?

The reply to that query will largely rely upon if you happen to’re responding to an ongoing local weather concern otherwise you’re pressured to reply to an occasion, says Andrew Jakabovics, vice chairman for coverage improvement at Enterprise Neighborhood Companions and co-author of “Housing Markets and Local weather Migration,” by the City Institute, an financial and social coverage suppose tank.

The Council on International Relations (CFR), an impartial suppose tank, says local weather change-fueled disasters are growing migration worldwide. CFR finds most migration happens inside nationwide borders, however cross-border migration is anticipated to rise. On the finish of 2022, 8.7 million folks worldwide — 675,000 within the U.S. alone — had been dwelling in inner displacement on account of weather-related disasters, in accordance with the Inside Displacement Monitoring Centre (IDMC). From 2008 to 2022, 11.1 million folks had been displaced within the U.S. on account of weather-related disasters, the IDMC discovered.

Chronically worsening situations — annual wildfires, hurricanes, warmth waves and floods — could not essentially destroy your property, however they’re definitely going to impression your life. Consultants say excessive climate occasions are those that make it tougher to face your floor.

“We’re not well-evolved by way of our reasoning to form of take into consideration low-probability however very high-impact occasions,” says De Sherbinin. “We are able to react when one thing huge occurs and determine, ‘Oh, God, that was actually means an excessive amount of,’ however we’re not well-evolved to handle issues which are form of steadily altering over time.”

A girl drinks amongst sand dunes close to an indication warning of maximum warmth hazard on the eve of a day that would set a brand new world warmth report in Loss of life Valley Nationwide Park on July 15 close to Furnace Creek, California. (Picture by David McNew/Getty Photos)

And for individuals who already dwell in high-risk areas, their single largest funding is their house, says De Sherbinin. And so they’re not going to go away simply “as a result of flood danger has risen from one in 100 years to at least one in 10 years,” he says. “They simply roll the cube and determine that out later. Or they’ll foyer to get their authorities to construct the required infrastructure to guard them.”

When folks do go away, they not often go far. The Dialog, a nonprofit information group largely written by lecturers and researchers, mapped out the place folks transfer following flooding disasters by FEMA’s Hazard Mitigation Grant Program from 1990 to 2017. It’s a buyout program that pays householders to buy and demolish flood-damaged houses. The info reveals that irrespective of the place the flooding occurred, most householders who took a buyout stayed shut by — simply 7.Four miles was the median distance. Three in 4 folks stayed inside 20 miles of their authentic houses.

Amongst those that do go away, usually familial ties and communal ties drive relocation selections, says Jakabovics. “When you’re leaving the island of Puerto Rico, there was a form of a preexisting inhabitants in components of Florida. That was in no way the one geography that individuals moved to, however there was a focus there,” says Jakabovics.

There are additionally individuals who, even within the occasion of a catastrophe, wish to return to their houses as a result of, understandably, it’s their house. At that time, habitability turns into a query of security compliance, insurance coverage and extra. When you’re not a house owner and also you wish to return, it’s possible you’ll face an excellent greater problem.

“When you’re a renter, proper, you may have little or no management over the bodily state of the property. And so, it relies on what the owner has to or can do,” says Jakabovics. “We all know that post-Hurricane Katrina, loads of the rental inventory was uninhabitable and a number of the new insurance coverage necessities and issues like that made it very, very tough to maintain these properties liveable.”

After all, the longer you wait to go away a high-risk space, the more difficult it could be. “As a substitute of a form of orderly, considerate course of, which Individuals have a really onerous time with, folks might be shedding their shirts,” says Pincetl.“They will not have the ability to promote their properties.”

Is wherever actually protected to dwell?

Nowhere is solely protected to dwell, however some areas might be much less liable to sure disasters than others. Warmth is most excessive within the southern states, and particularly in probably the most arid areas; flooding is worse alongside the coasts and close to giant our bodies of water; and tornadoes are extra widespread within the Nice Plains. The San Andreas fault stretches alongside your complete California coast, whereas different, smaller fault traces are unfold all through the west. The best-threat volcanoes sit alongside the West Coast of the continental U.S., in addition to Alaska and Hawaii. No place is immune.

Whether or not you may go someplace “safer” will rely in your monetary scenario. For hundreds of thousands of Individuals who dwell in poverty, the extra related query is more likely to be, “Can I afford to go?”

Populations which are extra typically affected by and fewer in a position to face up to the well being impacts of local weather change embrace older adults, youngsters, low-income communities and a few communities of coloration, in accordance with a 2018 authorities report referred to as the “Fourth Nationwide Local weather Evaluation.”

Leaving one space for an additional will at all times be simpler for these with the monetary sources to take action. When excessive climate or a pure catastrophe hits, these with better socioeconomic challenges have much less capability to go away. And so they’ll additionally bear the brunt of worsening climate situations to return.

METHODOLOGY

NerdWallet drew the checklist of fastest-growing counties utilizing 2021-2022 information from the U.S. Census Bureau, the latest accessible information set. The fastest-growing counties on this checklist had been restricted to the highest 10. The fastest-growing counties are these with the very best numeric inhabitants will increase over a set interval. The 10 counties had been then matched with their corresponding dangers utilizing the Federal Emergency Administration Company Nationwide Threat Index and FEMA’s historic information for catastrophe declarations from 1953 onward.

(Lead photograph by Mario Tama/Getty Photos Information through Getty Picture)